.avif)

The Financial Crimes Enforcement Network (FinCEN) has issued a landmark final rule aimed at increasing transparency and combating money laundering in the U.S. residential real estate sector. Effective December 1, 2025, this rule introduces new reporting requirements for certain non-financed transfers of residential real property to legal entities and trusts. The move is a direct response to the growing use of opaque ownership structures and all-cash transactions by illicit actors seeking to launder funds and evade detection.

NETBankAudit experts have over 25 years of experience in BSA/AML audits and compliance. If you have any questions after reading this guide, please reach out to our team.

Understanding the Scope and Purpose of the Final Rule

Why FinCEN Is Targeting Non-Financed Transfers

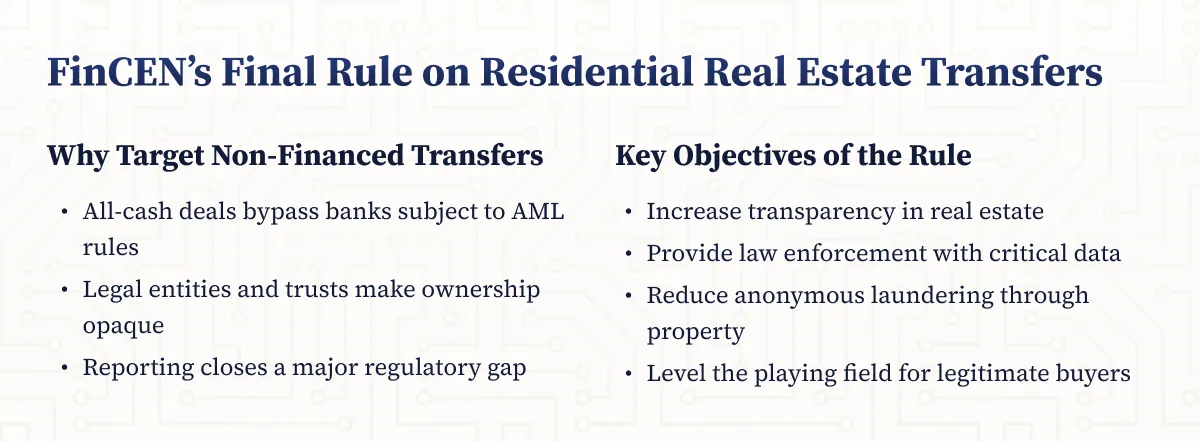

Illicit actors frequently exploit non-financed (all-cash) real estate transactions, especially when property is acquired through legal entities or trusts. These transactions bypass the scrutiny of financial institutions, which are subject to anti-money laundering (AML) and countering the financing of terrorism (CFT) program requirements and Suspicious Activity Report (SAR) obligations under the Bank Secrecy Act (BSA). By requiring reporting on these high-risk transactions, FinCEN aims to close a significant regulatory gap and provide law enforcement with critical data to identify and disrupt money laundering schemes.

Read FinCEN’s Final Rule Fact Sheet on Residential Real Estate Transfers

Key Objectives of the Rule

- Increase transparency in the residential real estate sector.

- Assist law enforcement and national security agencies in identifying illicit finance risks.

- Reduce the ability of criminals to anonymously launder proceeds through real estate.

- Level the playing field for individuals and small businesses competing in the U.S. economy.

What Transactions Are Reportable?

Defining a Reportable Transfer

A Real Estate Report must be filed for any non-financed transfer of an ownership interest in residential real property to a transferee entity or transferee trust. The rule applies regardless of the value of the property or whether consideration is exchanged, gifts are included. However, transfers made directly to individuals are not covered.

For additional answers to commonly asked questions, read FinCEN’s Residential Real Estate FAQs.

Residential Real Property Includes:

- Single-family houses, townhouses, and condominiums (including units in large buildings).

- Cooperatives and shares in cooperative housing corporations.

- Vacant or unimproved land where the transferee intends to build a one-to-four family residence.

- Mixed-use properties, such as a residence above a commercial enterprise, if designed for one-to-four families.

Non-Financed Transfers Defined

A non-financed transfer is one that does not involve an extension of credit to all transferees that is both:

- Secured by the transferred property, and

- Extended by a financial institution subject to AML program and SAR requirements.

If a private lender or non-bank finances the transaction, it is still considered non-financed for the purposes of this rule.

Exemptions: What Is Not Reportable?

To reduce compliance burden and focus on higher-risk activity, the rule exempts several types of transfers:

- Grants, transfers, or revocations of easements.

- Transfers resulting from death (including by will, trust, operation of law, or contractual provision).

- Transfers incident to divorce or dissolution of marriage/civil union.

- Transfers to bankruptcy estates.

- Transfers supervised by a U.S. court.

- No-consideration transfers by an individual (or with their spouse) to a trust where they are the settlor/grantor.

- Transfers to a qualified intermediary for a like-kind exchange under Section 1031 of the Internal Revenue Code.

- Transfers for which there is no reporting person (i.e., none of the specified professionals are involved).

Who Must File: The Reporting Person and the Cascade System

Determining the Reporting Person

Only one business is responsible for filing the Real Estate Report for each reportable transfer. The rule uses a “cascade” system to determine which professional involved in the transaction is responsible:

- The person listed as the closing or settlement agent on the closing/settlement statement.

- If none, the person who prepares the closing/settlement statement.

- If none, the person who files the deed or other instrument with the recordation office.

- If none, the person who underwrites an owner’s title insurance policy for the transferee.

- If none, the person who disburses the greatest amount of funds in connection with the transfer.

- If none, the person who provides an evaluation of the status of the title.

- If none, the person who prepares the deed or other legal instrument transferring ownership.

If none of these functions are performed, no report is required.

Designation Agreements: Flexibility for Industry

To reduce burden and provide flexibility, professionals involved in the cascade may enter into a written designation agreement to assign reporting responsibility to another party in the cascade. Each agreement must be unique to the transaction and retained for five years by all parties to the agreement.

%201%20(1).svg)

%201.svg)

THE GOLD STANDARD INCybersecurity and Regulatory Compliance

What Information Must Be Reported?

Required Data Elements

The Real Estate Report must include:

- Identifying information about the reporting person.

- Details about the transferee entity or trust (including legal name, address, and taxpayer identification number).

- Identifying information for beneficial owners of the transferee entity or trust (name, date of birth, address, citizenship, TIN).

- Information about individuals signing documents on behalf of the transferee.

- Information about the transferor (seller or grantor).

- Details about the property (address, legal description, date of closing).

- Total consideration paid and details about payments (method, amount, payor, account information).

Beneficial Ownership: Key Definitions

- Transferee Entity: Any individual who exercises substantial control or owns/controls at least 25% of the entity’s ownership interests.

- Transferee Trust: Any individual who is a trustee, has authority to dispose of trust assets, is a sole beneficiary with rights to income/principal, is a grantor/settlor with revocation rights, or is a beneficial owner of an entity/trust holding one of these positions.

Reasonable Reliance and Certification

Reporting persons may generally rely on information provided by others, unless they have reason to doubt its reliability. For beneficial ownership information, the reporting person may rely on information provided by the transferee or their representative, but only if it is certified in writing as accurate to the best of their knowledge. This certification must be retained for five years.

Reporting and Recordkeeping Requirements

Filing Deadlines and Procedures

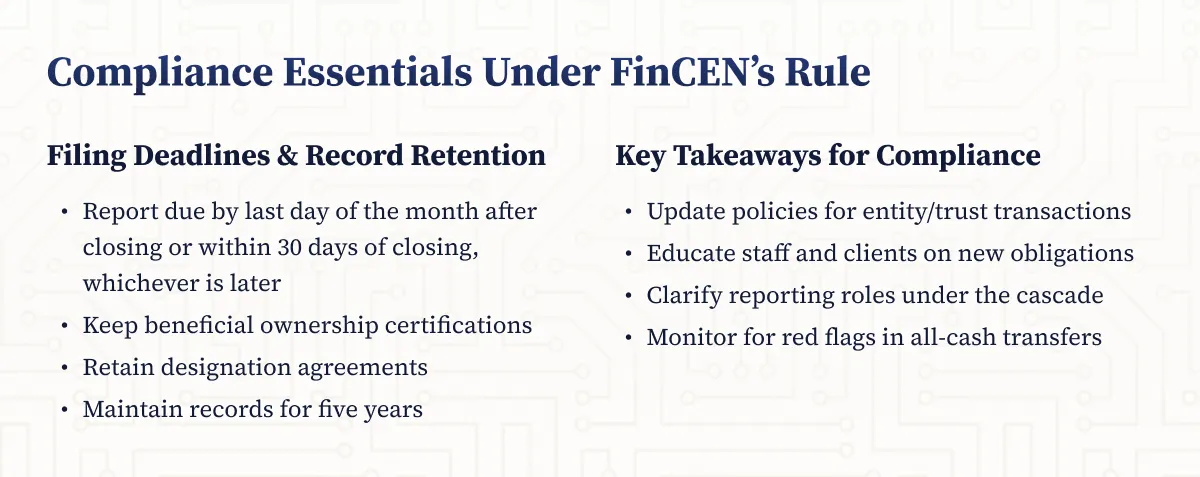

A Real Estate Report must be filed by the later of:

- The last day of the month following the month in which the closing occurred, or

- 30 calendar days after the date of closing.

FinCEN will provide a secure electronic filing system for these reports. The reports will not be accessible to the public and will be protected under strict confidentiality protocols.

Record Retention

Reporting persons must retain:

- A copy of the beneficial ownership certification form (signed by the transferee or their representative).

- Any designation agreement entered into for the transaction.

These records must be kept for five years. There is no requirement to retain a copy of the filed Real Estate Report itself.

Compliance Considerations for Financial Institutions

Impact on Compliance Programs

The rule does not require reporting persons to implement a full AML/CFT compliance program. However, compliance professionals should ensure that their real estate clients and business partners are aware of these new obligations and are prepared to collect, verify, and retain the required information.

Key Takeaways for Compliance Professionals

- Review and update policies and procedures for real estate-related transactions involving legal entities and trusts.

- Educate staff and clients about the new reporting requirements and the importance of beneficial ownership transparency.

- Coordinate with real estate professionals to clarify roles and responsibilities under the cascade and designation agreement options.

- Monitor for potential red flags in non-financed real estate transfers, especially those involving complex ownership structures.

How NETBankAudit Can Help

As the regulatory landscape for real estate transactions evolves, financial institutions and their compliance teams face new challenges in managing risk and ensuring adherence to FinCEN’s requirements. NETBankAudit offers specialized BSA/AML audit and consulting services tailored to the needs of banks, credit unions, and other financial institutions. Our team brings over 25 years of experience in regulatory compliance, risk assessment, and internal controls.

- Expert Guidance: We help you interpret and implement the latest FinCEN rules, including the new real estate reporting requirements.

- Policy & Procedure Review: Our experts assess your current compliance framework and recommend updates to address new risks.

- Training & Education: We provide targeted training for your staff and clients on beneficial ownership, reporting obligations, and red flag identification.

- Audit & Assurance: NETBankAudit’s independent audit services help you identify gaps, test controls, and prepare for regulatory examinations.

Request a proposal from NETBankAudit today to ensure your institution is ready for the new era of real estate transparency and compliance.

.svg)

%201.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.png)

.webp)

.webp)

.webp)

.webp)

%201.webp)

.webp)

%20(3).webp)

.webp)

%20Works.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%201.svg)