.avif)

What is the Status of CFPB and Other Regulatory Agencies?

Community financial institutions in the United States are operating within a dynamic and complex regulatory environment. This landscape is shaped by evolving supervisory priorities, political shifts, and the ongoing challenges of balancing compliance with operational efficiency. As a partner with over 800 organizations, primarily community financial institutions that are supervised by a variety of federal and state regulators, NETBankAudit has observed the changing regulatory environment and is actively working with our clients to help them respond appropriately. This article summarizes our observations and suggestions for navigating this dynamic environment.

Assessment of the Current Environment

Under the current White House administration, bank regulation is undergoing significant shifts aimed at reducing regulatory burdens on financial institutions, rolling back consumer protection measures, and consolidating oversight functions. Specific examples include the reversal of several existing consumer protection rules. For instance, the administration recently scrapped a rule that capped credit card late fees at $8, arguing that it violated the Credit Card Accountability and Disclosure Act of 2009. Additionally, with respect to overdraft fees, a bill repealing a rule that limited overdraft fees to $5 has passed both the House and Senate. These actions reflect a broader rollback of consumer protection initiatives, including efforts to reduce the scope of the Consumer Financial Protection Bureau.

Status of the Consumer Financial Protection Bureau

As of April 2025, the Consumer Financial Protection Bureau (CFPB) is navigating a period of significant upheaval, marked by legal challenges, administrative restructuring, and political contention. The changes began in January 2025, when President Donald Trump appointed Treasury Secretary Scott Bessent as the Acting Director of the CFPB. The subsequent nomination of Jonathan McKernan to serve as CFPB Director is pending confirmation; however, this suggests a potential shift toward a more lenient regulatory environment for community banks. It is also noted that the Department of Government Efficiency (DOGE) attempted to dismantle the agency by closing its headquarters and directing staff to cease operations.

%20Status.webp)

These actions led to legal interventions; notably, U.S. District Judge Amy Berman Jackson issued an injunction in March 2025, mandating the reinstatement of terminated employees and halting further efforts to dismantle the agency. This dynamic situation has also introduced uncertainty and operational pauses at the CFPB, leading to potential delays or shifts in compliance expectations.

The CFPB's future remains uncertain. While judicial interventions have temporarily preserved its operations, the agency faces continued political and administrative pressures. The outcome of ongoing legal battles and administrative decisions will significantly influence the CFPB's capacity to fulfill its mandate of safeguarding consumer financial interests.

Status of Other Federal Regulatory Agencies

The changes at the CFPB are not the only significant developments in financial services regulation. All of the federal financial institution regulatory agencies are undergoing substantial restructuring in response to a new focus on efficiency and reduction in regulatory burden. Specifically, in response to concerns about regulatory complexity, federal bank regulatory agencies have initiated efforts to review and potentially reduce outdated or unnecessary regulations. The following summarizes recent changes at the respective departments and agencies.

Federal Reserve

As of April 2025, the Federal Reserve's supervision of financial institutions is undergoing significant changes, influenced by leadership transitions, evolving regulatory priorities, and legal challenges from the banking industry. In February 2025, Michael S. Barr stepped down as the Federal Reserve's Vice Chair for Supervision, citing concerns over potential disputes distracting the Fed's mission. His resignation came ahead of President Donald Trump's return to office, which could have led to conflicts given Trump's deregulatory stance. President Trump has nominated Governor Michelle Bowman to succeed Barr. Bowman, a former community banker and Fed board member since 2018, has pledged to reform the Fed's oversight of large banks and promote "pragmatic" financial regulation. She advocates for simplifying the complex and overlapping regulatory framework, easing burdens on smaller banks, and improving transparency and clarity from bank supervisors.

The Federal Reserve continues to supervise a range of financial institutions, including bank holding companies, savings and loan holding companies, state member banks, and foreign banking organizations. Supervision is tailored based on the size and complexity of each institution. Key supervisory priorities continue to include Liquidity and Credit Risk Management, Cybersecurity, and Novel Activities Supervision.

Office of the Comptroller of the Currency

As of April 2025, the Office of the Comptroller of the Currency (OCC) has implemented significant changes in its supervision of financial institutions, reflecting a shift towards modernization and regulatory recalibration. The OCC's Fiscal Year 2025 Bank Supervision Operating Plan, effective from October 1, 2024 to September 30, 2025, outlines a risk-based supervisory approach. This strategy emphasizes early identification of material and emerging concerns, requiring banks to take timely corrective actions to maintain safety and soundness. The OCC has categorized its supervisory priorities into three main areas: Financial Risk, Operational Risk, and Compliance Risk.

%20Changes.webp)

In March 2025, the OCC announced the removal of "reputation risk" from its examination criteria and guidance materials. This decision aims to enhance transparency and focus supervisory efforts on quantifiable risks that directly impact an institution’s financial condition. Additionally, the OCC has eased certain restrictions on digital asset activities. A new interpretative letter permits nationally chartered banks to engage in cryptocurrency-related services, such as custody and participation in distributed ledger networks, without prior approval. However, banks are expected to maintain robust risk management controls for these activities.

Rodney E. Hood assumed the role of Acting Comptroller of the Currency in February 2025. Under his leadership, the OCC has withdrawn from the Network of Central Banks and Supervisors for Greening the Financial System, citing that climate change falls outside the agency's statutory responsibilities. Hood has also advocated for regulatory sandboxes to foster innovation in the banking sector. The OCC's current supervisory framework reflects a balance between fostering innovation and ensuring financial stability. By focusing on quantifiable risks, embracing technological advancements, and adjusting regulatory approaches, the agency aims to maintain the integrity and resilience of the national banking system.

Federal Deposit Insurance Corporation

As of April 2025, the Federal Deposit Insurance Corporation (FDIC) is undergoing significant changes in its supervision of financial institutions, reflecting a shift towards streamlined regulation, increased transparency, and a focus on core financial risks. Under the leadership of Acting Chairman Travis Hill, appointed in January 2025, the FDIC has outlined new priorities emphasizing a departure from previous regulatory approaches. Hill has indicated a focus on encouraging de novo bank formations, promoting innovation, and conducting a comprehensive review of existing regulations to eliminate redundancies and outdated guidance.

In line with its new direction, the FDIC has rescinded several policies from the previous administration, including the 2024 Bank Merger Policy Statement. Additionally, the agency has delayed compliance dates for certain provisions related to official signs and advertising requirements, providing institutions with more time to adapt. The FDIC has also clarified its stance on crypto-related activities. In recent guidance, the agency rescinded previous requirements for FDIC-supervised institutions to obtain prior approval before engaging in permissible crypto-related activities, streamlining the process while maintaining oversight.

The FDIC is facing operational challenges, including staffing shortages and an aging workforce. A 2024 report highlighted that 36% of the agency's workforce is expected to be retirement-eligible by 2027, exceeding government-wide averages. In response, the FDIC is seeking to reduce its workforce by an additional 20% as part of a broader government initiative led by the Department of Government Efficiency (DOGE). The FDIC's current supervisory approach reflects a balance between fostering innovation and ensuring financial stability. By focusing on core financial risks, adjusting regulatory frameworks, and addressing operational challenges, the agency aims to maintain the integrity and resilience of the national banking system.

National Credit Union Administration

As of April 2025, the National Credit Union Administration (NCUA) continues to adapt its supervisory framework to address evolving risks and ensure the stability of the credit union system. The agency's 2025 Supervisory Priorities highlight key areas of focus, reflecting both ongoing challenges and emerging concerns. The NCUA's 2025 Supervisory Priorities, outlined in Letter 25-CU-01, emphasize the following areas: Credit Risk, Liquidity Risk, Consumer Financial Protection, Cybersecurity, and Interest Rate Risk. In December 2024, the NCUA Board approved changes to the examination scheduling policy, effective January 1, 2025. These adjustments aim to provide more flexibility and efficiency in the examination process, allowing the agency to better allocate resources based on risk profiles.

Current Areas for Regulatory Focus

With the changing regulatory landscape, most community financial institutions are looking for direction regarding the areas of focus for their next examination. NETBankAudit has observed that the following topics are currently receiving the most attention by the regulators.

- Fair Lending and Community Reinvestment Act (CRA) Compliance: Regulators continue to prioritize fair lending practices, with a particular emphasis on preventing redlining and ensuring equitable access to credit. The modernization of the CRA, finalized in 2023, encourages community financial institutions to expand services in low- and moderate-income communities and adapt to technological changes. Most requirements become applicable by 2026, prompting institutions to prepare for enhanced reporting and compliance measures.

- Anti-Money Laundering (AML) and Financial Crimes Compliance: Community financial institutions are under increased scrutiny regarding AML practices. Regulators are focusing on enhanced customer due diligence and beneficial ownership reporting. The integration of artificial intelligence is being explored to improve transaction monitoring and risk assessment, aiming to detect suspicious activities more effectively.

- Cybersecurity and Data Privacy: With the rise of digital banking and remote work, community financial institutions face heightened cybersecurity risks. Regulators are emphasizing stricter compliance requirements to protect consumer data, urging institutions to bolster their cybersecurity frameworks to prevent breaches and safeguard sensitive information.

- Current Expected Credit Losses (CECL) Implementation: Regulators are closely examining community financial institutions’ implementation of the CECL accounting standard. Institutions are expected to refine their processes for estimating credit losses, ensuring that methodologies are robust and reflective of current economic conditions.

- Regulatory Tailoring and Oversight: The U.S. Treasury and Federal Reserve have signaled a shift towards more tailored regulatory approaches for community financial institutions. Treasury Secretary Scott Bessent advocates for commonsense regulations that alleviate undue burdens on smaller banks, promoting a more transparent and efficient oversight framework. Similarly, Federal Reserve Governor Michelle Bowman emphasizes simplifying the regulatory framework to ease burdens on smaller financial institutions and enhance clarity.

- Basel III Endgame Considerations: The upcoming implementation of the Basel III Endgame reforms, set to begin in July 2025 with a three-year phase-in period, has raised concerns among community financial institutions. There is apprehension that these international standards may impose disproportionate capital requirements on smaller institutions, potentially impacting their lending capabilities and operational flexibility.

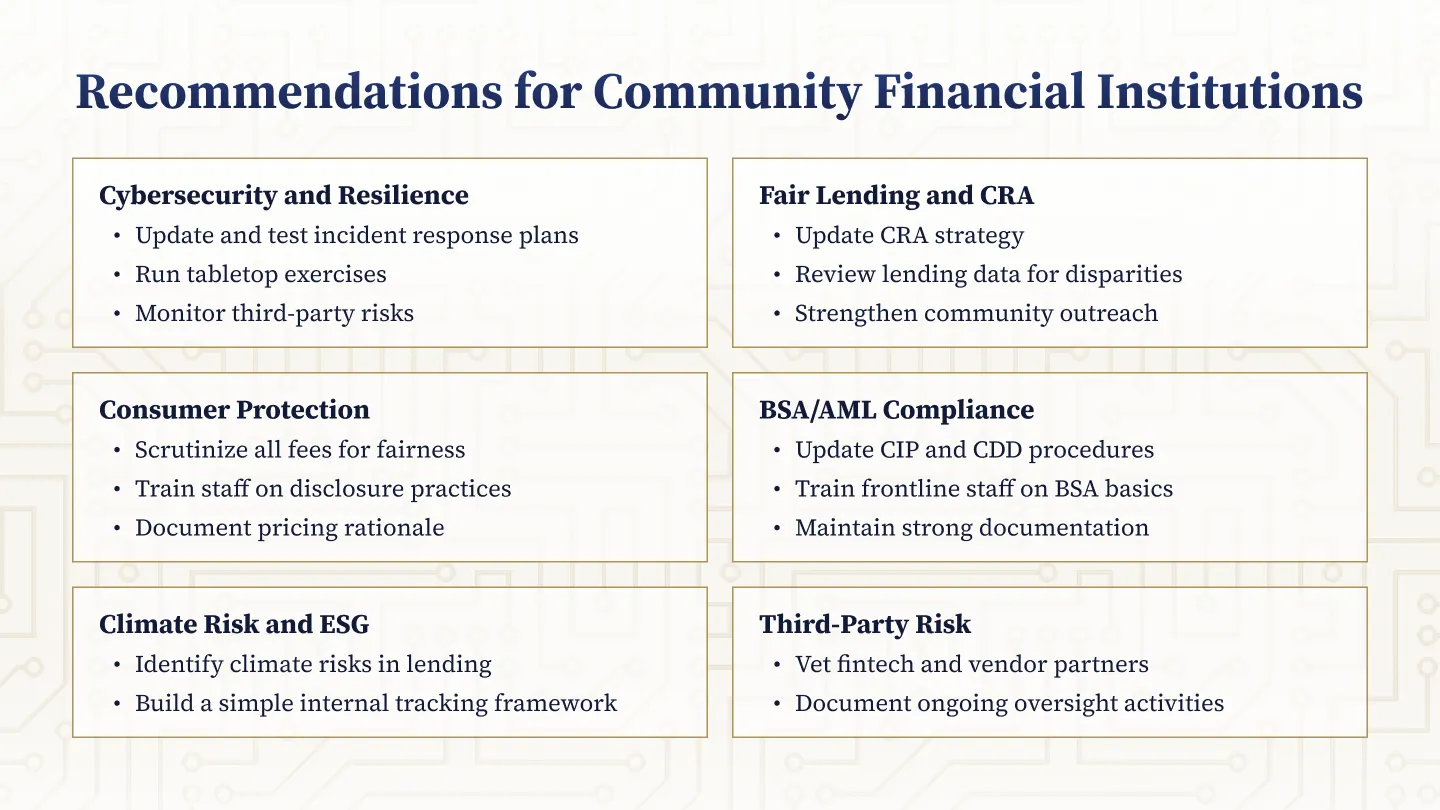

Recommendations for Community Financial Institutions

In this dynamic regulatory landscape, community financial institutions must remain vigilant and proactive, adapting to changes while continuing to serve their communities effectively. To navigate the current regulatory environment effectively, community financial institutions should focus on the following areas.

Cybersecurity and Operational Resilience:

- Ensure your incident response plan is current and tested.

- Run tabletop exercises.

- Document everything - Especially how you detect, escalate, and respond to incidents.

- Don’t ignore third-party risk - Vendors can be your weak link.

Fair Lending and CRA Modernization:

- Update your CRA strategy to reflect new assessment criteria.

- Review your lending data for potential redlining or pricing disparities.

- Stay proactive on community outreach.

Consumer Protection: Junk Fees, UDAP/UDAAP:

- Scrutinize all consumer fees - Are they clearly disclosed? Reasonable? Avoidable?

- Train frontline staff on how to communicate fee structures.

- Document the rationale behind your pricing model.

Bank Secrecy Act / Anti-Money Laundering (BSA/AML):

- Update your CIP (Customer Identification Program) and CDD (Customer Due Diligence) procedures.

- Educate relationship managers on BSA/AML compliance basics.

- Don’t over-collect information, but make sure your documentation is airtight.

Climate Risk and ESG (Environmental, Social, Governance):

- Begin identifying climate-related risks in your loan portfolio.

- If you're lending heavily in agriculture or coastal real estate, know your exposures.

- Keep a simple internal framework - Risk identification, assessment, and monitoring.

Third-Party Risk and Fintech Partnerships:

- Vet your partners like you would an internal operation.

- Make sure your board understands the risks and benefits of these relationships.

- Document ongoing oversight.

The current regulatory environment is dynamic as economic, political, and technological factors are introducing numerous opportunities and challenges. However, community financial institutions can continue to succeed and serve their customers by staying informed of these changes and responding in a timely manner.

%201%20(1).svg)

%201.svg)

.svg)

%201.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.png)

.webp)

.webp)

.webp)

.webp)

%201.webp)

.webp)

%20(3).webp)

.webp)

%20Works.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%201.svg)