.avif)

The Financial Crimes Enforcement Network (FinCEN) is rapidly reshaping the regulatory landscape for virtual assets and cryptocurrency mixing services. As the U.S. Treasury prepares to apply the PATRIOT Act to virtual assets and targets crypto mixers for potential bans or severe restrictions, compliance professionals at financial institutions face a new era of regulatory scrutiny, technical complexity, and risk management challenges. This article provides a detailed analysis of FinCEN’s evolving approach, the compliance obligations for financial institutions, and actionable strategies to mitigate risk in this dynamic environment.

NETBankAudit experts have over 25 years of experience in virtual asset and BSA/AML audits and compliance. If you have any questions after reading this guide, please reach out to our team.

Regulatory Evolution: From Interpretive Guidance to Section 311 Actions

FinCEN’s Early Virtual Asset Oversight

FinCEN’s regulatory journey with virtual assets began in 2013, when it issued its first interpretive guidance clarifying that entities accepting and transmitting virtual currency are subject to Bank Secrecy Act (BSA) requirements as money transmitters. This foundational guidance established the distinction between “users,” “administrators,” and “exchangers,” setting the stage for subsequent compliance obligations and regulatory interpretations.

Expansion and Clarification: 2013–2019

Between 2013 and 2019, FinCEN refined its approach through administrative rulings and consolidated guidance, addressing emerging business models such as peer-to-peer exchangers, wallet providers, and decentralized applications. The 2019 guidance was pivotal, consolidating prior rulings and clarifying that BSA obligations apply based on the function performed, not the technology used.

Proactive Enforcement and the Travel Rule

A significant shift occurred in 2019 when FinCEN explicitly applied the Travel Rule to all convertible virtual currencies, requiring the collection, retention, and transmission of originator and beneficiary information for transactions exceeding $3,000. This move signaled a more proactive enforcement posture, with the IRS citing Travel Rule violations as the most common deficiency among virtual asset money services businesses.

Section 311 and the Focus on Crypto Mixers

The most dramatic regulatory development came in October 2023, when FinCEN invoked Section 311 of the USA PATRIOT Act to propose designating transactions involving crypto mixers as a primary money laundering concern. This marked the first time FinCEN targeted a class of transactions, rather than specific institutions or jurisdictions, reflecting the unique risks posed by anonymity-enhancing technologies.

Current Regulatory Framework for Virtual Assets

Money Transmitter Status and BSA Obligations

Under FinCEN’s framework, any entity that accepts and transmits convertible virtual currency (CVC) is likely a money transmitter, subject to BSA registration, anti-money laundering (AML) program requirements, recordkeeping, and reporting obligations. This includes exchanges, hosted wallet providers, and payment processors handling virtual assets.

Travel Rule Compliance

The Travel Rule, extended to virtual assets in 2019 and updated in 2024, requires financial institutions to collect and transmit originator and beneficiary information for transactions over $3,000. Implementing this rule for virtual assets is technically challenging due to the decentralized nature of blockchain networks and the prevalence of unhosted wallets.

Customer Due Diligence and Enhanced Monitoring

Financial institutions must implement robust customer identification programs, ongoing monitoring, and enhanced due diligence for higher-risk customers and activities. This includes leveraging blockchain analytics, wallet clustering, and transaction tracing to identify suspicious patterns and connections to illicit activities.

Crypto Mixers: Regulatory Focus and Section 311 Authority

Why Mixers Are in the Crosshairs

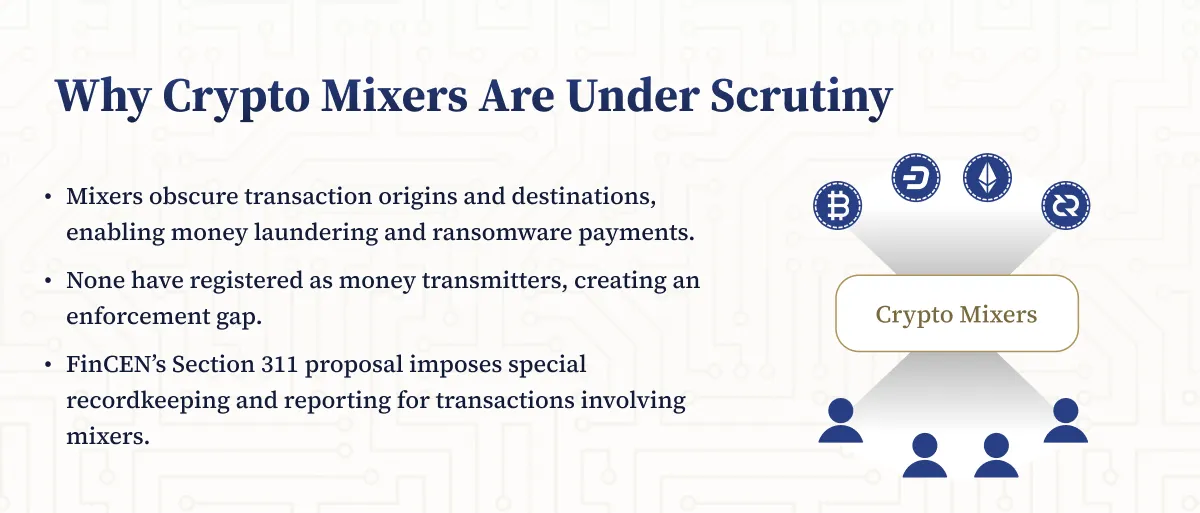

Crypto mixers intentionally obscure the origin and destination of virtual asset transactions, making them attractive tools for money laundering, ransomware groups, and state-sponsored cyber actors. FinCEN’s analysis found that no mixers had registered as money transmitters, creating a regulatory gap exploited by criminals.

Section 311 Designation: Scope and Impact

FinCEN’s proposed rule under Section 311 would require financial institutions to implement special recordkeeping and reporting for transactions involving mixers, especially those with foreign jurisdictional connections. The definitions of “CVC Mixer” and “CVC Mixing Service” are broad, potentially capturing decentralized finance (DeFi) protocols, cross-chain bridges, and smart contract-based exchanges.

Key Compliance Implications

- Institutions must identify and report transactions involving mixers, even indirectly through customer activity.

- Enhanced monitoring and blockchain analytics are required to detect mixing patterns across multiple networks.

- Failure to comply can result in civil penalties, criminal prosecution, and reputational damage.

Enforcement Actions and Market Impact

Major Enforcement Milestones

FinCEN’s $60 million penalty against the operator of Helix and Coin Ninja in 2020 set a precedent for aggressive enforcement against unregistered mixing services. The Treasury’s Office of Foreign Assets Control (OFAC) has sanctioned major mixers like Blender.io and Tornado Cash, effectively removing them from the legitimate financial ecosystem.

Coordinated Government Response

Recent actions such as the Department of Justice’s prosecution of Samourai Wallet demonstrate a coordinated approach across regulatory and law enforcement agencies.These actions have had a chilling effect on privacy-focused crypto services, though new alternatives continue to emerge.

Market and Institutional Response

Financial institutions have responded by enhancing transaction monitoring, implementing stricter onboarding for virtual asset clients, and leveraging advanced analytics to detect indirect exposure to mixers. The message is clear: institutions must be able to identify and report suspicious activity, even when not directly interacting with mixing platforms.

Technical and Operational Compliance Requirements

Blockchain Analytics and Transaction Monitoring

Effective compliance requires integrating blockchain analytics platforms capable of tracing transactions, identifying wallet clusters, and flagging interactions with high-risk addresses or services. These systems must operate across multiple networks and provide real-time monitoring to support timely reporting.

Customer Identification and Enhanced Due Diligence

Institutions must verify customer identities, assess wallet ownership, and document the source of funds for virtual asset transactions. Enhanced due diligence is essential for customers with high transaction volumes, cross-border activity, or connections to higher-risk jurisdictions.

Travel Rule Implementation Challenges

Implementing the Travel Rule for virtual assets requires systems that can collect, retain, and transmit required information, even when dealing with unhosted wallets or non-compliant counterparties. Collaboration with other institutions and service providers is critical to ensure compliance.

Recordkeeping, Reporting, and System Integration

Recordkeeping systems must accommodate blockchain data formats and support efficient retrieval for audits or regulatory inquiries. Regulatory reporting systems should be enhanced to include blockchain transaction identifiers, wallet addresses, and other virtual asset-specific data elements.

Cybersecurity and Staff Training

Virtual asset operations introduce new cybersecurity risks, including threats to wallet addresses, private keys, and transaction data. Institutions must implement robust security frameworks and provide ongoing training to ensure staff are equipped to manage these risks.

.webp)

Risk Assessment and Management Frameworks

Comprehensive Risk Assessment

Financial institutions must develop risk assessment frameworks that address the unique risks of virtual asset activities, including money laundering, terrorist financing, and exposure to high-risk jurisdictions. This includes evaluating customer profiles, transaction patterns, and counterparty relationships.

Technology and Counterparty Risk

Evaluating the security and compliance of blockchain networks, smart contracts, and third-party service providers is critical. Institutions must assess the adequacy of vendor compliance programs and monitor regulatory violations or enforcement actions.

Emerging Risk Identification

Given the rapid evolution of virtual asset technologies, institutions must establish processes to identify and respond to new risks, including those associated with DeFi protocols, cross-chain bridges, and decentralized exchanges.

%201%20(1).svg)

%201.svg)

THE GOLD STANDARD INCybersecurity and Regulatory Compliance

Emerging Challenges: DeFi and Decentralized Services

Regulatory Gaps and Decentralization

Decentralized finance (DeFi) protocols often operate without centralized control, complicating the application of BSA/AML requirements. FinCEN has indicated that DeFi services accepting and transmitting virtual assets likely qualify as money transmitters, but true decentralization may place some activities outside current regulatory coverage.

Effective Control and Compliance

Determining whether a DeFi protocol is subject to regulation depends on whether individuals or entities retain control over smart contracts or protocol governance. Institutions must analyze protocol architecture and control structures to assess compliance obligations.

Cross-Chain Bridges and DEXs

Protocols facilitating asset transfers across blockchains or enabling decentralized trading present additional compliance challenges. Institutions must monitor customer interactions with these services and assess associated risks.

Practical Compliance Recommendations for Financial Institutions

To navigate the evolving regulatory landscape, financial institutions should implement the following strategies:

- Establish robust governance and oversight: Designate experienced compliance officers and ensure board-level engagement in virtual asset risk management.

- Develop comprehensive policies and procedures: Address all aspects of the customer lifecycle, including onboarding, monitoring, and escalation for suspicious activities.

- Integrate advanced blockchain analytics: Select platforms that provide real-time monitoring, risk scoring, and investigative capabilities across multiple networks.

- Enhance staff training: Provide ongoing education on virtual asset technologies, regulatory requirements, and investigation techniques.

- Strengthen vendor management: Conduct enhanced due diligence on third-party service providers and monitor compliance with regulatory standards.

- Regularly test and audit compliance programs: Evaluate the effectiveness of controls, monitoring systems, and reporting processes through independent testing.

- Prepare for incident response: Establish clear procedures for investigating and remediating compliance violations, including voluntary disclosure and corrective action.

- Maintain business continuity plans: Address operational risks unique to virtual asset technologies, including network disruptions and regulatory changes.

Partner with NETBankAudit for Virtual Asset Compliance Excellence

As FinCEN’s regulatory framework for virtual assets and crypto mixers continues to evolve, financial institutions must adapt quickly to remain compliant and competitive. NETBankAudit offers specialized BSA/AML, virtual asset, and cybersecurity audit services tailored to the unique challenges of digital asset compliance. Our team brings decades of experience, deep regulatory insight, and advanced technical expertise to help your institution:

- Assess and enhance your virtual asset compliance program

- Implement effective blockchain analytics and transaction monitoring

- Navigate complex regulatory requirements, including the Travel Rule and Section 311 actions

- Prepare for regulatory examinations and independent audits

- Train staff and develop robust governance frameworks

Contact us for an RFP for our virtual asset compliance solutions. Stay ahead of regulatory change and protect your institution from emerging risks.

.svg)

%201.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.png)

.webp)

.webp)

.webp)

.webp)

%201.webp)

.webp)

%20(3).webp)

.webp)

%20Works.webp)

.webp)

.webp)

%20(1).webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

.webp)

%201.svg)